Is the 50/30/20 Rule Still Relevant? How the Stoa Saving Score Helps You Save Better

A simple idea that’s somehow survived everything

Let’s be honest — budgeting advice hasn’t exactly evolved at the speed of the rest of finance. Fintech is full of crypto dashboards and robo-advisors, yet many people are still walking around trying to guess how much to spend or save each month.

That’s where the 50/30/20 rule comes in.

It’s a budgeting framework that’s been around for decades — popularised by US Senator Elizabeth Warren — and it breaks your monthly income down into three neat categories:

- 50% on needs: rent, groceries, utilities

- 30% on wants: restaurants, subscriptions, holidays

- 20% on savings or debt repayments

It’s clear, actionable, and surprisingly hard to stick to.

But at Stoa, we believe it’s still one of the most powerful ideas in personal finance — if we reframe how it’s applied, track it properly, and design for real behaviour (not just best-case scenarios).

So that’s what we did.

Why people are still drawn to 50/30/20

What’s interesting is how many UK financial institutions still use this rule in their education content — from HSBC and Halifax to Lloyds and Co-operative Bank.

There’s good reason: it’s intuitive.

At a glance, it helps you separate:

- Survival from lifestyle

- Impulse from intention

- Spending from growth

In an age of subscription creep and lifestyle inflation, even just asking “Is this a need, a want, or something I should be saving?” is a powerful mental model.

But here’s the catch: it’s aspirational — not realistic for everyone.

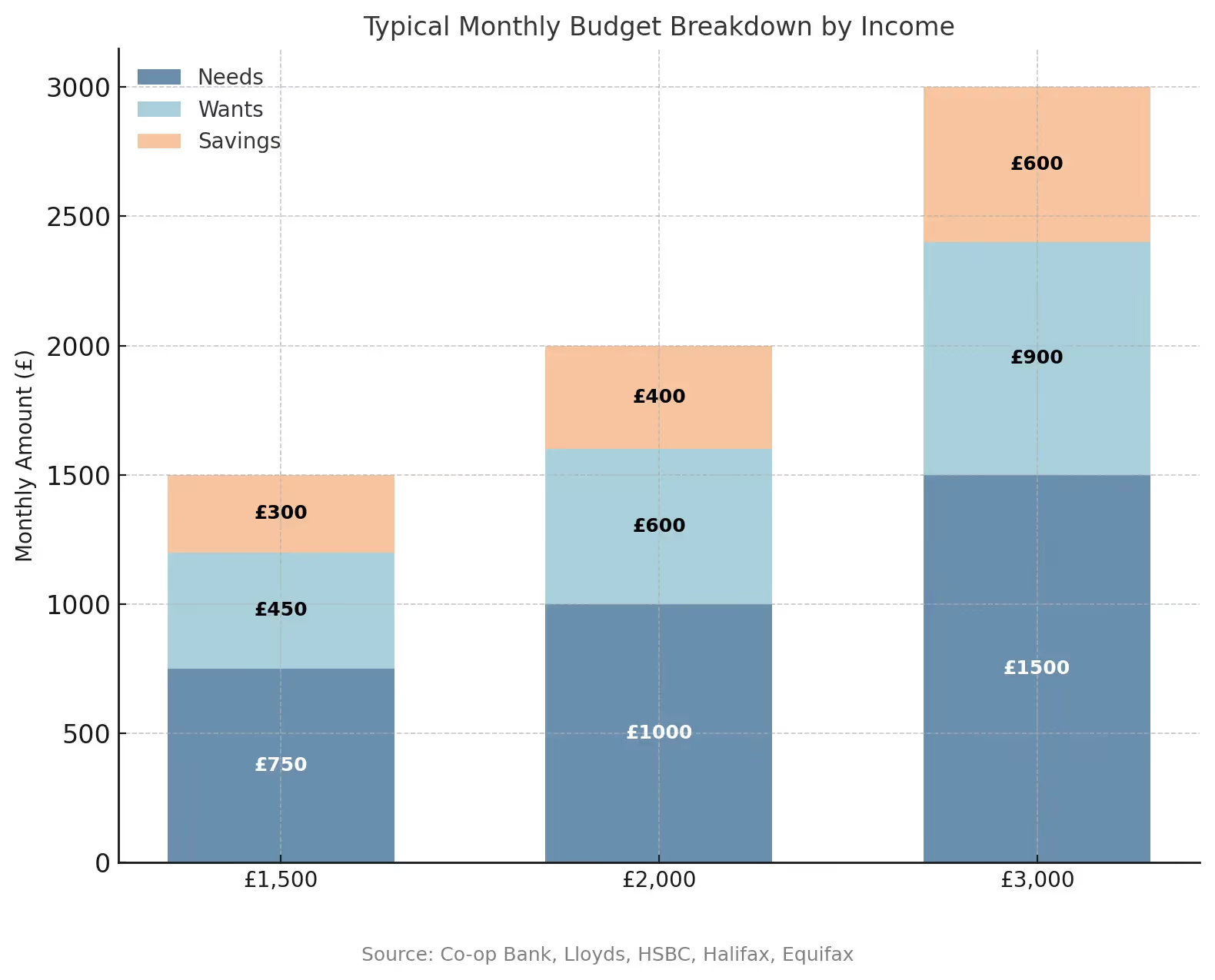

London, meet your enemy: fixed costs

According to The Telegraph, a typical London earner bringing in £2,700 post-tax might already be spending 65% or more on essentials — rent, council tax, food, commuting.

.avif)

That leaves less than 10% for savings, if anything at all.

So if you’ve tried 50/30/20 and it’s felt out of reach — you’re not alone. Your spending isn’t broken. The model just needs to flex.

The real insight? It’s not about hitting those numbers. It’s about tracking behaviour and slowly nudging it in the right direction.

The rise of the aspirational spender

It’s not just rent that throws the 50/30/20 rule off.

Enter the aspirational spender: the creative freelancer or startup lead earning decent money — but with equally ambitious lifestyle goals. Organic meal kits, £90 wellness retreats, finance coaching apps, high-end gym memberships.

This group isn’t reckless. They’re optimistic. They invest in themselves. But they also tend to overspend on “wants” thinking they’re “needs.”

Stoa insight: Our Saving Score algorithm often flags this drift — not to punish it, but to help rebalance it.

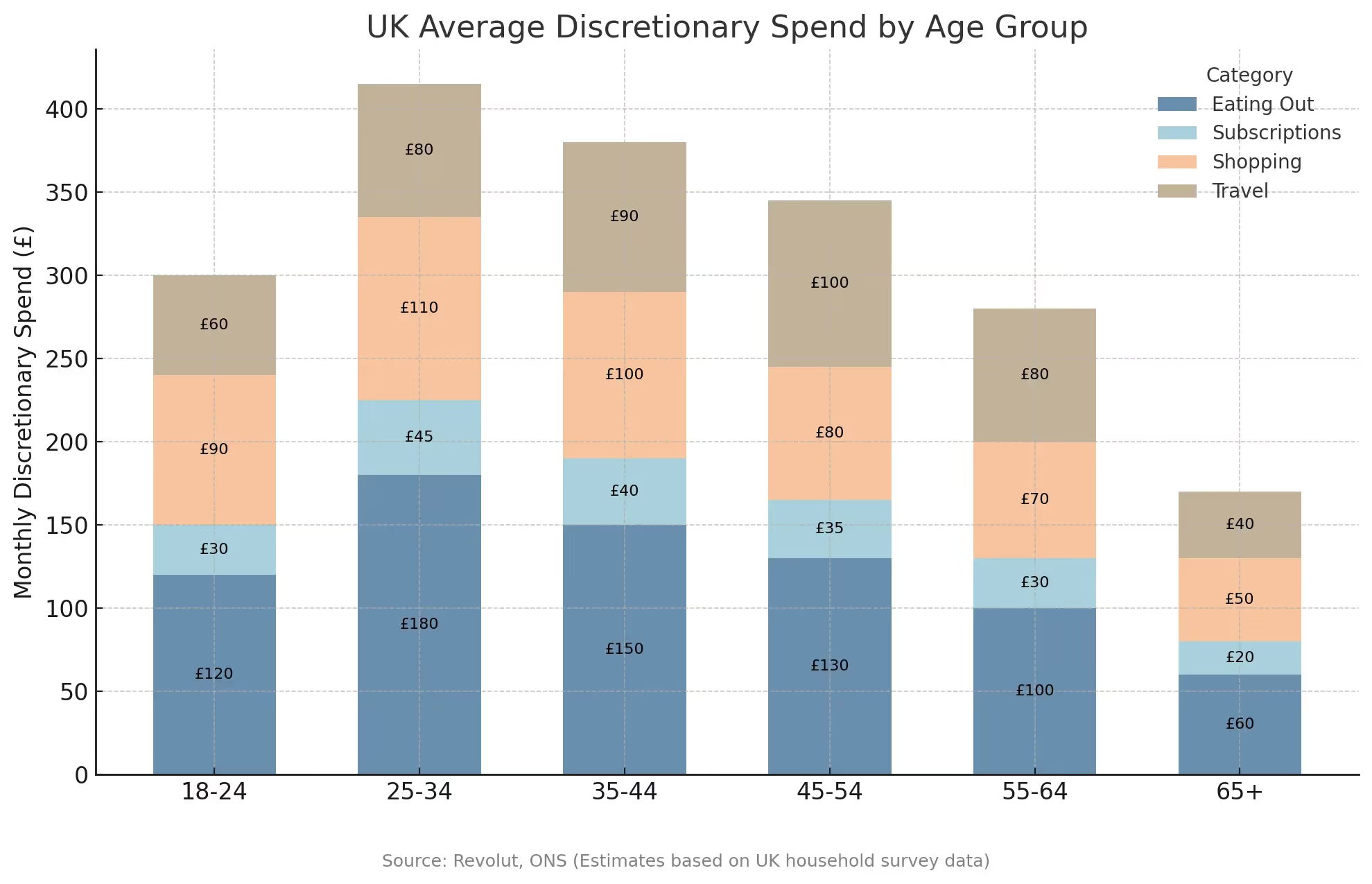

The age gradient of wants vs. needs

Your age has a major influence on how your budget actually gets allocated.

According to ONS and Revolut data:

- Under 30s spend more on travel, takeaways, and subscriptions

- Over 45s shift spending toward healthcare, home maintenance, and debt repayment

- Across all age groups, “wants” often exceed the recommended 30%

That’s not necessarily a problem. But again — awareness is everything. You can’t change what you don’t track.

Most people save less than 10% — and that’s okay

Money.co.uk’s 2024 survey found:

- 1 in 4 UK adults save less than 5% of their monthly income

- The average monthly saving is just £234

- The most common monthly saving amount is £50–100

.avif)

Even though the rule says 20%, the reality is much closer to 8–12%. And that's before you factor in unexpected costs like dental work, broken boilers, or childcare emergencies.

💥 Budgeting Myths We Need to Let Go Of

❌ “I can’t budget until I earn more.”

Budgeting is about awareness, not wealth. Start where you are.

❌ “If I can’t hit 20%, I’ve failed.”

Start with 5%. Build momentum. Progress compounds.

❌ “Wants are bad.”

Wants are joy. Just don’t let them take over the whole pie.

❌ “I don’t need to save yet.”

Future-you will thank you if you start today.

❌ “Budgeting means cutting back on everything.”

Nope. It means intentionality — spending without guilt because the basics are sorted.

What makes saving stick? Psychology, not spreadsheets.

Behavioural economists like Kahneman and Thaler have shown us just how irrational we are — and how to design for it.

At Stoa, we built the Saving Score around three key behavioural truths:

- Default Bias — We’re more likely to save when it’s automatic. (Thaler & Sunstein – Nudge)

- Loss Aversion — We hate losing more than we love winning. So we frame poor saving as “missing out” on future freedom. (Kahneman & Tversky – Prospect Theory)

- Immediate Gratification — We crave short-term wins. So we designed the score to update monthly — like a financial fitness tracker. (Benartzi & Thaler – Save More Tomorrow)

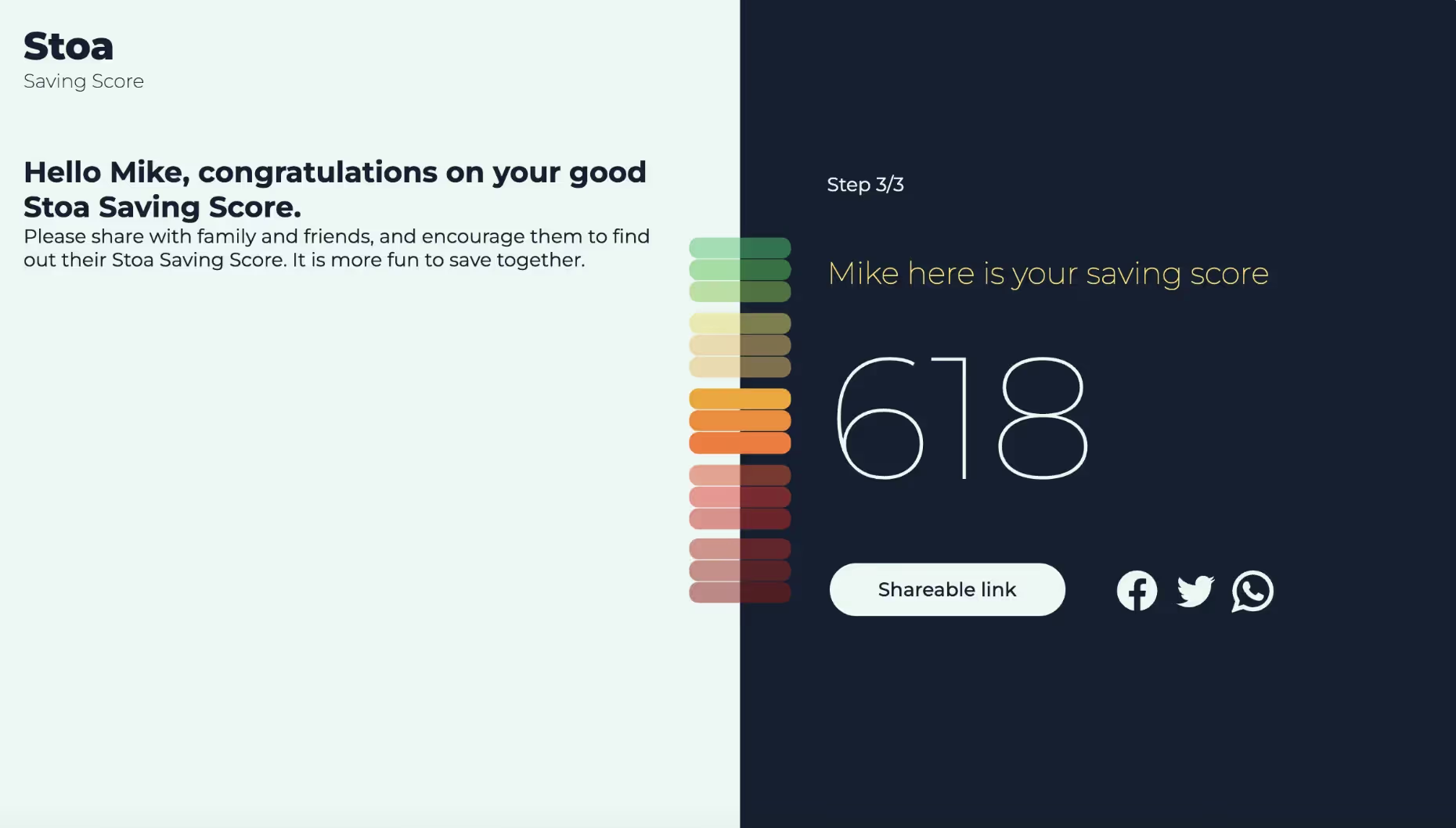

🔍 So, What Actually Is the Stoa Saving Score?

Think of the Stoa Saving Score as a behaviour-first lens on your financial life.

It’s not about how much you’ve saved — but how well you’re saving.

The score is grounded in three pillars:

- Income Retention — How much of your income do you actually keep after expenses? This pillar looks at your ability to create surplus — the gap between what you earn and what you spend.

- Savings Allocation — Once you’ve retained some of your income, where does it go? Do you direct it towards long-term savings, short-term goals, or just let it sit idle?

- Saving Regularity — This is the big one. Anyone can save once. But do you do it again? This pillar tracks the consistency of your saving behaviour over time.

Together, these three factors build a clearer picture of your financial habits — and unlock your monthly Stoa Saving Score, powered by UK bank data and Open Banking.

No judgment. No credit impact. Just clarity.

Why 50/30/20 is still a good starting point

The rule gives you structure without rigidity. And in a world where financial anxiety is rising (hello cost of living crisis), structure is what helps us breathe.

Even if your actual split looks more like:

- 60/25/15 (inner city rent)

- 70/20/10 (high debt repayment)

- 45/35/20 (dual-income household with fixed expenses)

…the point isn’t how you divide it. It’s that you’re thinking in ratios, not just receipts.

So where do you start?

Here’s the playbook we recommend — no matter your salary, age, or postcode:

- Audit your spending – even just once

- Sort by needs, wants, and savings (your bank app may help)

- Look at the ratio — not just the raw numbers

- Try saving 10% first — then build to 20%

- Use tools like the Stoa Saving Score to track your trend

- Don’t aim for perfection — aim for consistency

Stoa exists not to judge your financial life — but to reflect it back to you in a way that helps you grow.

Final thoughts: This is about agency, not austerity

The best budgeting system is the one that helps you live better — not spend less out of guilt.

The 50/30/20 rule works because it gives your money purpose. And the Stoa Saving Score builds on that by giving your savings momentum.

So whether you’re an overstretched renter or a high-earning optimist, the best time to start tracking your habits was last year. The second best time is now.

🔁 Ready to check your Saving Score?

Get your free score in under 60 seconds at www.SavingScore.com

No paperwork. No credit impact. Just a better way to see how your saving habits stack up — and how to improve them.

Learn More About Stoa

We at Stoa are on a mission to make savings fun.